2025 Medical Plans: When you enroll in the Choice HSA Plan or Kaiser HMO with HSA, you can open a Health Savings Account (HSA) with Fidelity which is funded by you. An HSA is a tax-free savings account* that works with a qualified health plan to help you pay your plan deductible and qualified out-of-pocket healthcare expenses. Refer to IRS Publication 502 for a complete list of eligible expenses.

Opening Your Fidelity HSA

Follow these steps to open your Fidelity HSA:

- Watch for an email (or postcard mailed to your home if you don’t have an email address on file in Workday) from Fidelity with information on how to open your new Fidelity HSA.

- After you receive the email or postcard from Fidelity, log in to netbenefits.com (the same website used for our 401(k)). If you don’t have a netbenefits.com account setup already, you will be prompted to create an account.

- Once you are logged in to the Fidelity website, click on the link to Open Your HSA. If you have questions, call Fidelity at 800-544-3716.

NOTE: You must open your HSA online through netbenefits.com. You cannot open your HSA over the phone. Open your HSA by January 1, 2025 to ensure your account can receive your first January, 2025 contribution.

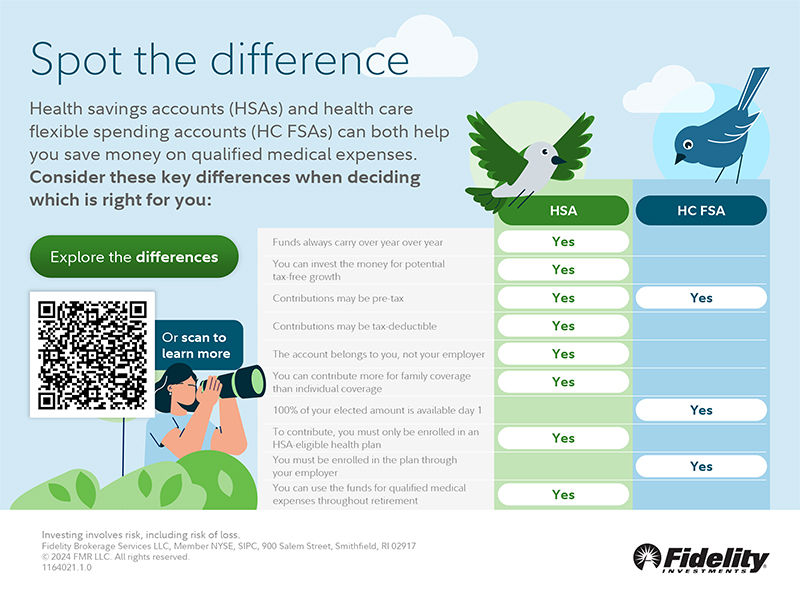

Download an HSA flyer with the steps required to open an HSA with Fidelity.

Transferring Your Existing HSA Balance from HealthEquity to Fidelity

If you have a balance in your existing HealthEquity HSA and would like to transfer it to Fidelity, you can begin the process after January 6, 2025.

Follow these steps:

- Go to www.fidelity.com/toa. You will need your most recent HealthEquity account statement available and will need to upload it to Fidelity as part of the balance transfer process.

- If your HealthEquity HSA balance is invested, you will need to liquidate your investments and move them to the cash account. Invested funds cannot be transferred to Fidelity.

- Once a completed online form has been submitted to Fidelity, the transfer process from HealthEquity to Fidelity takes 3 to 4 weeks. You can track the progress of the transfer via www.fidelity.com.

There is a $25 fee assessed by HealthEquity to transfer assets to Fidelity. If you enrolled in the HSA during Open Enrollment for 2025 and complete the transfer of assets between January 1 and March 31, 2025, Fidelity will make a $25 adjustment to your Fidelity HSA to cover this fee. The adjustment will appear in your account by the end of May, 2025 and will not count towards annual deferral limits.

NOTE: You have the option to leave your existing HSA at HealthEquity; however if you decide to do this, you will be charged a $3.95 monthly individual account fee starting February 1, 2025.

Download an HSA flyer with the steps you need to take to transfer an existing HSA balance from HealthEquity to Fidelity.

Do You Have a Personal HSA?